Ieri è uscito l’ISM manifatturiero di Febbraio.

Dichiarazioni assai ottimistiche della stampa :

[…]Economic activity in the manufacturing sector expanded in February for the seventh consecutive month, and the overall economy grew for the 10th consecutive month.[…]

Ed in effetti il dato, sia pure in leggera contrazione e sotto un consensus troppo ottimistico, sembrerebbe decisamente buono :

C’è però da notare che i dati di inventario stanno contraendosi – ed in una vera espansione economica ciò non dovrebbe succedere – e che soprattutto questi dati risentono ancora degli stimoli statali.

Ed inoltre , è interessante notare leggendo fra le righe questo :

[…]lead times for electronic parts are pushing out to 8 to 24 weeks.(Computer & Electronic Products)[…]

Questo semplicemente significa che il comparto tech – al di là delle dichiarazioni e delle cifre ottimistiche riportate nelle ultime settimane – non crede che questa ripresa sia sostenibile a lungo, altrimenti le scorte di magazzino sarebbero molto più grandi.

In ogni caso , dal punto di vista tecnico non devono essere sottovalutati i segnali che ci arrivano dai mercati, che confermano per il momento una visione rialzista degli indici principali.

Infatti lo S&P500 si riporta sopra la media a 50gg, con spazi di risalita che – almeno tecnicamente – appaiono interessanti.

Mentre il DXY continua a mostrare – anche se a mio modo di vedere solo momentaneamente – tutta la sua forza :

Interessante – a conferma di ciò che sto vedendo da tempo – che il vero movimento di forza dell’USD sia nel Cable con il GBP, oltre ad una marcata debolezza della £ contro tutte le valute mondiali, in particolare l’AUD ed il CAD (ieri -3% contro entrambe le divise).

Come ben ricorderete, al di là delle bizzarre dichiarazioni che appaiono sulla stampa e che non vale la pena commentare per quanto siano assolutamente fuori da ogni logica, ho segnalato già dalla scorsa settimana che la BOE ha di fatto già iniziato il QE 2.0, unito ad una svalutazione della propria moneta (e segnalo un’altra volta che diversi titoli del FTSE100 sono ai massimi storici come quotazione).

Questo fatto è da tenere a mio avviso molto in considerazione, perchè ci mostra lo scenario che verrà.

Nel frattempo, la speculazione sull’€/$ deve essere – ma solo momentaneamente – interrotta, ed allora si deve trovare qualcuno a cui rifilare il pacco (= violento short covering).

Ecco perchè tutti ora ne parlano, e si sentono le ipotesi più fantasiose :

[…]Certainly sovereign CDS traders can not be far behind (especially those who traded with a less than bullish bias over the past month) from the wrath of the Greek, Spanish and British secret services, and now – various US legal and criminal administrations, which are currently convinced that it is just speculators who are at fault for 15 years of fraudulent eurozone budgetary presentations and countless bond offerings based on fake financials, finally coming to the fore.

Seriously, sell anything, and you will soon be facing the business end not of misdemeanor, but real-deal felony charges, and possibly with sprinkles of treason to boot.[…]

Quando iniziano a circolare voci su servizi segreti, spy-story e simili (perchè, nessuno è al corrente di ciò che sta succedendo ?), è proprio il momento che si andrà nella direzione opposta a quella attesa.

Giova però ricordare che ieri per l’ennesima volta abbiamo raggiunto l’ennesimo record per il Gold, ma in € (ed anche rispetto – ovviamente – alla £) :

E gli interessi richiesti dagli istituzionali per il bailout greco sono talmente alti (e – purtroppo – a ragione, vista la situazione disperata) da non credere, il 7% su base annua, roba da terzo mondo :

[…]For now, the tensions over Greece haven’t locked it out of the debt markets, provided it’s willing to pay up, said Michiel De Bruin at F&C Investments.

“We would consider participating in the new bond sale if there’s a good premium” over existing debt, said De Bruin, who helps manage $28 billion of assets as head of euro government bonds at the Amsterdam-based firm.

“If they show progress on cutting the deficit, people will be more comfortable with Greek risk,” he said.

De Bruin estimates the country will have to pay a so-called spread of 30 basis points to 50 basis points more than the yield on its current 10-year benchmark bond, which traded at 6.38 percent on Feb. 26, according to data compiled by Bloomberg.[…]

E Golden Slacks, pardon Goldman Sachs, che sta facendo in questo momento ?

Stanno naturalmente gufando.

Ed iniziano a pubblicare scalette temporali sui prossimi ultimatum :

[…]Given all the rumours flying around today on Greece and the possible financing, a number of people have asked me to update my “Greek roadmap” for the next three critical months that I have circulated on earlier occasions.

As a reminder, Greek PM Papandreou said last week that the government is funded through mid-March; the press has reported that they are contemplating a 10-year bond issuance to get through May, and a number of European politicians have hinted at a bail out plan being prepared in case its needed, possibly in the order of EUR20-25bn, and possibly via bond placement with state-owned institutions, including KfW in Germany.

Our view has long been that IF official money will be needed, then it’ll come very late in the game, and not “pre-emptively”, and that it’ll be relatively short term money (maybe 6-months money) bridging the Greek government over the April-May hump.

Here is what we know:

March 5:

PM Papandreou meets with German chancellor Merkel in Berlin. (If I were to be wrong on the issue of the EU not offering them “pre-emptive” financing, I would be absolutely shocked if such pre-emptive financing were to come ahead of this meeting.)

March 9:

PM Papandreou meets with US president Obama in Washington. (This is a long planned meeting and entirely unrelated to the financial crisis.)

March 10:

EUR1.65bn in coupon payments.

March 15:

Deadline for the Greek government to spell out the implementation deadline for the additional measures discussed last week with the delegation from the Commission, ECB and the IMF, and to be fine-tuned this week in meetings with Commissioner Rehn.

These are likely to include a 2% increase in the VAT rate, further increases in fuel surcharges, a doubling to 20% in cuts in supplemental income, as well as further cuts on the pension front. There are also discussions of further structural measures, including the abolishment of the present layoffs legislation that limits layoffs to 2% of the workforce.

March 16:

Ecofin and Eurogroup meetings to evaluate the measures.

Second half of March:

If the government has not been able to raise the necessary funds in the commercial market during the first half of March, then this would be the most likely period for the Euro-zone governments to pull the bazooka out – in the form of implementing art 122. I suspect that the money would be relatively short term (six months or so).

March 20:

Coupon payments

April 20:

EUR8.2bn in redemptions

May 19:

EUR8.1bn in redemptions[…]

Tutto vero, naturalmente, ma questo sembra più una scena da Final Countodown che un resoconto dettagliato della situazione.

Ma i profitti di GS vanno sempre di più in orbita, naturalmente :

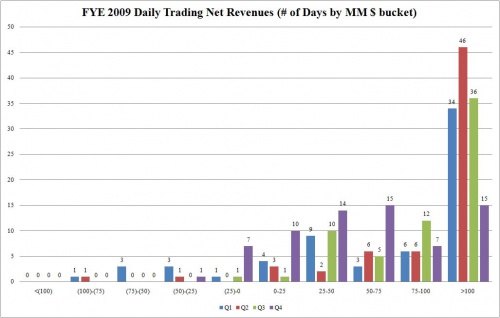

Complimenti, risultati sempre migliori, anche se finalmente un pochino più umani rispetto all’incredibile performance del Q3 :

[…]In Q3, Goldman reported just one days of losses in 65 total trading days, as well as 36 days of $100MM+ profits, in Q4 the distribution looks much more normal (if still massively skewed toward profitability).

In Q4 the firm announced it lost between $25 and $50 million once, lost under $25 million for 7 days, but most notably made over $100 million on “just” 15 days, a 58% decline from Q3.

The Q4 $100MM+ trading days represent just 11% of all 2009 $100MM+ trading days.

And here is an observation for you distributions fans: in 2009, Goldman made over $100MM on 131 out of 263 trading days, or 50%. It lost over $100MM on 0 out of 263 trading days, or 0%.[…]

Ancora complimenti.

Per concludere, una annotazione di carattere tecnico sulle commodities, ed in questo caso mi occupo del copper, la cui spike rialzista di ieri non è certo stata determinata da miglioramenti di carattere economico, ma dai tragici eventi cileni (ricordo che il Cile è uno dei maggiori produttori mondiali di rame, oltre al fatto che era uno dei paesi messo meglio sulla via della “vera” ripresa economica) :

Si sta creando una island reversal – che naturalmente necessita di conferme – configurazione molto bearish nel breve periodo, e che sarebbe – nel caso fosse confermata nei prossimi giorni dagli eventi – un ulteriore campanello di allarme sulla sostenibilità della (virtuale) ripresa economica mondiale.