Indubbiamente la giornata di venerdì scorso è stata caratterizzata principalmente dal “Goldman Day”, che al momento non appare altro che la classica scusa per vendere un mercato tirato a palla come un elastico che naturalmente alla fine si è spezzato.

Un movimento atteso ed anticipato dalla pessima reazione del mercato alla trimestrale “normale” di Google (-7.6% alla fine) e da quella invece molto brillante di Intuitive Surgical (-7.12%).

Quindi il -11.98 % di GS in un contesto come questo non appare certo un movimento così drammatico, anche perchè tutto il comparto finanziario ha ceduto pesantemente (da ipercomprati francamente assurdi).

Solo per un giorno ?

Boh, chissà.

Ma intanto rivediamo in dettaglio quello che è successo venerdì pomeriggio a partire dalle 16 circa ore italiane :

The Securities and Exchange Commission today charged Goldman, Sachs & Co. and one of its vice presidents for defrauding investors by misstating and omitting key facts about a financial product tied to subprime mortgages as the U.S. housing market was beginning to falter.

The SEC alleges that Goldman Sachs structured and marketed a synthetic collateralized debt obligation (CDO) that hinged on the performance of subprime residential mortgage-backed securities (RMBS).

Goldman Sachs failed to disclose to investors vital information about the CDO, in particular the role that a major hedge fund played in the portfolio selection process and the fact that the hedge fund had taken a short position against the CDO.

“The product was new and complex but the deception and conflicts are old and simple,” said Robert Khuzami, Director of the Division of Enforcement.”

Goldman wrongly permitted a client that was betting against the mortgage market to heavily influence which mortgage securities to include in an investment portfolio, while telling other investors that the securities were selected by an independent, objective third party.”

The SEC’s complaint alleges that after participating in the portfolio selection, Paulson & Co. effectively shorted the RMBS portfolio it helped select by entering into credit default swaps (CDS) with Goldman Sachs to buy protection on specific layers of the ABACUS capital structure.

Given that financial short interest, Paulson & Co. had an economic incentive to select RMBS that it expected to experience credit events in the near future.

Goldman Sachs did not disclose Paulson & Co.’s short position or its role in the collateral selection process in the term sheet, flip book, offering memorandum, or other marketing materials provided to investors.

Il ruolo principale nella vicenda è ovviamente quello dell’hedge Paulson&C, che di fatto ha preso posizione immediatamente contro i prodotti venduti da GS agli ignari investitori (mai fidarsi di GS, se consiglia una cosa sicuramente sta facendo l’opposto nei suoi desks).

Ed infatti il movimento a mio avviso più significativo di venerdì è quello sul Gold, dove è nota a chiunque la netta esposizione long proprio dell’hedge di Paulson :

E se il grafico daily ci mostrerebbe una situazione ancora di uptrend :

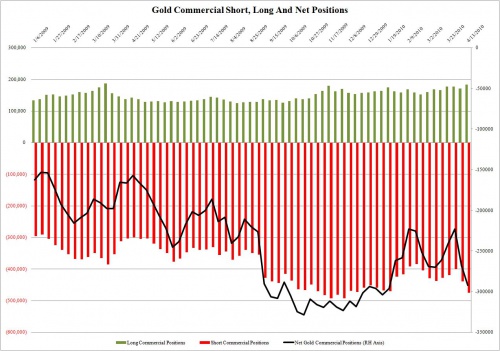

Gli istituzionali invece incrementano le loro posizioni al ribasso :

The just released CFTC Commitment of Traders indicates that the big banks increased their net short gold exposure to the highest since early 2010, hitting -292,244, a jump of -24,396, and an increase of -69,361 from two weeks prior.

Also, in the week ended April 13, the outright Commercial short positions in Gold hit a 2010 record.

Gold traders who observed this spike in commercial shorts, especially when combined with the surprising strong gold price action over the past two weeks, are concerned that the news about Goldman, and its ramifications on Paulson’s holdings of GLD, may have leaked over the past 10 days to allow banks to front-run today’s hit in the price of Gold.

The question of whether or not Paulson’s worries will materialize into an actual partial or full-scale liqudation will be an open ended question for some time: today many of the key Paulson positions, primarily in financials and commodities have gotten hit hard, leading many to believe that the market may force his hand.

Beh, naturalmente il problema è proprio questo, e le posizioni aperte sul future non hanno certamente una valenza di tipo fondamentale, ma di tipo prettamente pratico.

Ma la domanda più importante cui ci si dovrebbe chiedere è un’altra :

If the logic on the gold plunge is that Paulson will be dumping (as we first reported), that means that GGBs, in which Paulson has sizable long cash exposure (with or without the CDS), will be the next to go.And since he can’t hedge anymore (remember the whole thing about CDS speculators being branded traitors), he will be forced to sell.

Eh, sì, perchè come ben sappiamo, sia GS sia soprattutto l’hedge di Paulson sono direttamente coinvolti nella saga greca.

Ed appunto, se Paulson sarà costretto a liquidare tutto, dovrà anche svendere i suoi CDS greci in possesso.

Ma a chi ?

Forse a GS stessa, chissà.

In ogni caso, una situazione assai intricata, in cui si intrecciano non solo speculazioni contro GS, ma proprio da parte di GS stessa, che ovviamente sapeva da tempo di essere nel mirino della SEC.

Non ci credete ?

Leggete un po’ qua :

Time for the SEC to take a look at what bets Goldman’s prop desk, and material affiliates as well as hedge funds that are close to Goldman’s flow traders, were taking on Goldman’s stock over the past few days.

If indeed Goldman shorted itself, bought SPY puts, bought octuple leveraged negative financial ETFs, or something else of the sort, on material non-public information, it would be time to shut the firm down.

Perchè, ci sono dei dubbi a riguardo, soprattutto dopo che è venuto fuori questo, direttamente dalle grida :

Goldman sold 1,000 big SP today over 1,200.00. Was it just a hedge because they KNEW the SEC would do nail them to the cross ?

Is that insider trading ?

Who knows how many tens of thousands they sold in the ES?

Mica sarebbe strano, ma la normalità, diretta conseguenza del rialzo forzatissimo e soprattutto tiratissimo che abbiamo visto nell’ultima settimana.

Non è nè la prima, nè sarà l’ultima volta.

Per altro, ripeto, fare uscire la notizia della possibile frode di GS il giorno delle scadenze tecniche è un’altra perla da ricordare a lungo, esattamente come quella di febbraio in cui la FED alzo il costo del denaro il giovedì sera (giorno prima della scadenza tecnica di Febbraio) a mercati chiusi.

E naturalmente, di nuovo il solito algoritmo in azione :

La prossima fermata è a 1170, dove partirà presumibilmente la gamba di rimbalzo :

E che le posizioni long nella stragrande maggioranza nei casi siano state aperte indiscriminatamente senza alcuna protezione, lo dimostra la seguente analisi del Vix (oltre il fatto che il put/call ratio – come segnalato più volte negli ultimi giorni – aveva raggiunto valori non solo storicamente bassi, ma soprattutto stupidamente bassi) :

Non ci voleva molto a capirlo, bastava usare un po’ di logica, un po’ di esperienza e di senso critico per capire che la volatilità – in un senso o nell’altro – sarebbe esplosa a breve.

Mentre il reddito fisso – nel caso di rottura della resistenza (che non mi aspetto subito, ma al prossimo tentativo) avrebbe un buono spazio di salita, e coinciderebbe appunto con la correzione del 5-7% degli indici che mi aspetto nelle prossime settimane (al momento non di più, il quadro generale è tuttora bullish, ma naturalmente le sorprese possono stare dietro l’angolo).

Nel frattempo,è interessante vedere nei prossimi giorni il comportamento di tutto ciò che gira intorno alla galassia Goldman Sachs e sui financial USA in generale : i CDS relativi a GS sono improvvisamente saliti (solo speculazione ovviamente, probabilmente orchestrata dalla stessa GS) :

Goldman CDS 42 wider on the day, hits 133.

Has about 300 points to go before it surpasses Greece.

That said, the vampire squid is suddenly riskier than Russia (130), Brazil (115), Colombia (130), Thailand (115) and Italy (129).

Comico leggere che venerdì GS ha chiuso con un grado di rischio superiore a noi.

Per altro la capitalizzazione di GS si è improvvisamente ridotta, ma è sempre molto superiore ad esempio a quella di inizio dell’anno.

Ed il sell off, come fatto notare in precedenza, ha colpito non solo tutti i finanziari, ma è stato generalizzato : segno anche che il mercato cercava una scusa per essere venduto, a dispetto delle buone trimestrali viste fino a questo punto.

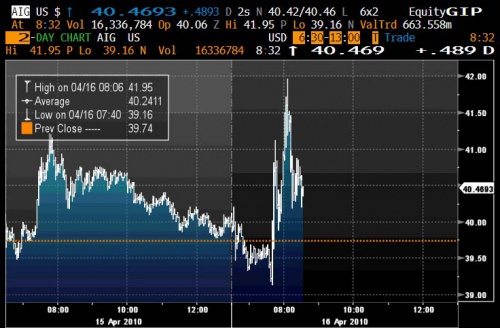

E che venerdì non si siano guardati i fondamentali, ma si sia mosso tutto esclusivamente sulla base della speculazione e basta, lo dimostra anche la spike in intraday di AIG, diretta concorrente – soprattutto in termini prettamente legali – di GS, dato che è probabile che AIG si beccherà a breve una bella class-action per le sue malefatte in giro per il mondo :