Oggi è il giorno del Non Farm Payroll, ma alcune indicazioni sul dato che uscirà questo pomeriggio le abbiamo già avute ieri con il Jobless Initial Claims, che si presta ad una lettura piuttosto interessante.

Apparentemente la situazione sembrerebbe migliorare sul fronte occupazionale USA.

Ma – se leggiamo i dati in maniera più approfondita :

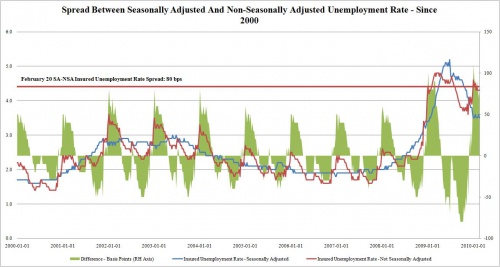

Vediamo che i dati stagionalizzati mostrano un miglioramento , ma quelli non stagionalizzati invece sono ancora in peggioramento.

Ed infatti :

Today’s BLS release on initial claims showed a moderate improvement in SA initial claims, which declined by29,000 from 498,000 to 469,000, which lead to a just noticeable improvement in the 4-week average, and a 134,000 decline in the SA unemployment to 4.5 million.

Yet this week once again saw a divergence between the SA and NSA numbers, where NSA initial claims increased by 17,128, and SA unemployed went up by 24,534 to 5.6 million. The spread in the SA and NSA unemployment rates, after tightening for 4 weeks, has once again started to diverge, and was at 80 bps, after hitting a 2010 tight of 70 bps in the week ended February 13.

Al di là di tutti i discorsi e di tutte le scuse che si possono portare (tempeste di neve, mese di Febbraio solo di 28 giorni) , è da rimarcare il fatto che gli USA – nonostante affermino che la recessione sia finita almeno da sei mesi a questa parte – continuano a perdere posti di lavoro.

E che la situazione non sia così buona come la propaganda vorrebbe dipingere, è abbastanza chiaro, basta leggere fra le righe le dichiarazioni che arrivano qua e là :

Moody’s Investors Service has today downgraded Deutsche Bank AG’s long-term deposit and senior debt ratings to Aa3 from Aa1, and its bank financial strength rating (BFSR) to C+ from B.At the same time, the long-term debt ratings of its rated branches and most of its subsidiaries were also downgraded.

Additionally, the ratings on the bank’s senior subordinated debt were downgraded to A1 from Aa2, and as a result of Moody’s revised Guidelines for Rating Bank Hybrids and Subordinated Debt, the bank’s trust preferred debt was downgraded to Baa1 from Aa3 (for cumulative instruments) and to Baa2 from Aa3 (for non-cumulative instruments). According to Moody’s, the downgrade of Deutsche Bank’s ratings primarily reflects a combination of three factors:

The continuing preponderance of capital market activities and the ensuing challenges for risk management which potentially expose the bank to earnings volatility that would be inconsistent with the bank’s previous ratings.

The delay in the acquisition of Deutsche Postbank AG (rated D+/A1) is set to defer the possible benefits of this acquisition beyond what was initially anticipated at the time when the rating agency changed the outlook to negative in December 2008.

Deutsche Bank’s other businesses, which had been expected to provide a more stable earnings anchor, have shown a greater degree of earnings volatility than Moody’s had previously expected

E’ vero che la credibilità di Moody’s è oramai nulla e che il downgrade di Deutsche Bank non è altro che fumo negli occhi di pessima qualità, ma le autorità tedesche hanno preso davvero sul serio questa barzelletta, prendendo delle comiche contromisure : il solito ban dello short selling sui finanziari tedeschi.

Investors whose net short positions, covered or uncovered, are more than 0.2% shares of an individual company will be required to disclose the information to the regulator under the new rules.

Positions of more than 0.5% will be published on the BaFin Web site without naming the holder.

The rule will be effective March 25, 2010, through Jan. 31, 2011.

After that period, the regulatory will re-examine the situation.

BaFin said the move was made necessity by the need for the regulator to be informed quickly to take “targeted action” should such activity pose risks.

Short-selling refers a trader selling shares not already owned with the idea of buying them back later at a lower price. This strategy is often used by institutional investors like hedge funds and can have destabilizing effect on the markets.

The 10 companies affected are: Aareal Bank AG (ARL.XE); Allianz SE (AZ); Generali Deutschland Holding AG; Commerzbank AG (CBK.XE); Deutsche Bank AG (DB); Deutsche Boerse AG (DB1.XE); Deutsche Postbank AG (DPB.XE); Hannover Re AG (HNR1.XE); MLP AG (MLP.XE); and Munich Re AG (MUV2.XE).

Dimostrando di non avere compreso nulla dalla lezione avuta nel 2008, quando contromisure di questo genere si sono dimostrate assolutamente insufficienti ed infondate, anzi , come ripeto da sempre – ma chi fa le leggi e sta nei board non ha mai fatto trading in vita sua – le ricoperture da short selling a volte sono davvero micidiali e distruttive più di ogni altra misura di protezionismo.

Eppure i tedeschi dovrebbero conoscere qualche cosa a riguardo, visto che proprio in Germania – nel 2008 , proprio mentre tutti i mercati stavano crollando – c’è stato il più ridicolo short squeeze della storia, quello su Volkswagen (per chi non si ricordasse questo fatto, basta andare nell’archivio del blog, dove è spiegato dettagliatamente quello che successe allora).

E nel frattempo, altra importante news proveniente dagli USA :

Market sources have cited a Fannie Mae business change that was said by sources to involve Fannie Mae restricting its non-US-bank lending in the fed funds rate market to the following list of 10 banks (US banks not changed): Deutsche Bank, ING, BNP, Barclays, Lloyds, RBS, Scotia, Ntl Bank of Canada, RBC and Toronto Dominion.Thus it would be “substantially reducing” its list of banks by “what was thought to be dozens” of banks, said a trader; it appeared there was no reason given.

Segno che qualcosa di importante sta per accadere in ambito interbancario, anche se non ci è dato conoscere la ragione di questo improvviso cambiamento di business da parte di FNM.

Improvviso stop alla liquidità fornita alle diverse banche che utilizzano programmi di High Frequency Trading nei diversi mercati, ad esclusione della lista fornita sopra ?

La saga greca ieri invece ha avuto una giornata di pausa , con la eccezione della seguente dichiarazione della BCE :

“The IMF technical assistance is very important, very appreciated, but the fact is that the conditionality inside the euro area has to be decided by the peers, according to the Stability and Growth Pact and the European framework as it stands.”

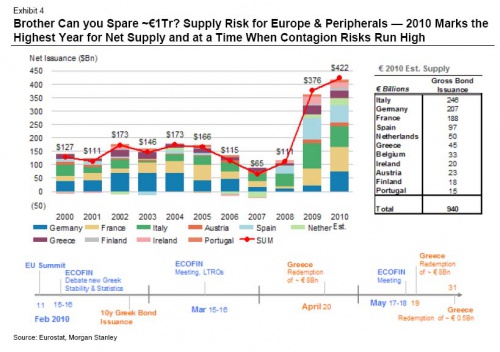

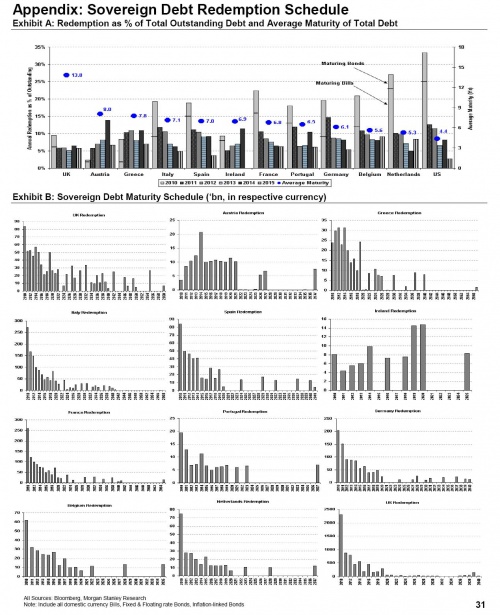

Ma la situazione dal punto di vista del debito in Europa pare molto difficile :

E soprattutto, se guardiamo la scadenza per l’anno in corso :

…è interessante notare questo “piccolo” problema :

[…]A detailed view of the redemption schedules in Europe (contrasted with the US) in absolute and relative terms yields the following charts. Italy, Spain, France, Germany, Portugal, Belgium and the Netherlands all have about 20%, and in some cases more, of their total debt maturing this year.

That’s some serious rolling. […]

Ed ecco allora perchè le parole di Marc Faber sulla situazione europea paiono appropriate :

[…]”I don’t think it will work out, and I think other countries like Spain and probably Portugal (and Italy) will then also have to be bailed out eventually, and it will lead to more monetization in Europe, one of the reason the euro has been so week…

The pain of the austerity will be very, very burdensome on Greece, and eventually the economy can not grow with the kind of budget they will have to enact, and under these conditions their currency is way overvalued (they are in the euro).And so without the ability to grow, their ability to pay the interest and repay the debt will actually diminish….

I think everybody should accumulate some gold over time. I would recommend people to buy every month some gold for ever.“[…]

Gold come unico investimento da cassetto per il lungo periodo (od in alternativa beni materiali) , esattamente quello che ho scritto nei giorni scorsi.

E le ragioni di questo fatto le spiega nel passo successivo :

[…]”Gold is not a liability of someone else, you really own it, you keep it in a safe deposit box, its quantity can not be increased at the same rate as you can print money which will eventually again weaken the US dollar.I am not saying that the dollar will go straight down, but eventually the purchasing power of money will lose […]

Perdita di potere di acquisto da parte della moneta, un altro tema a me caro e su cui insisto da mesi.

Ed infatti aggiunge :

[…]If you compare the depression years, in the depression years we did not have credit cards and we did not have unfunded liabilities from Social Security, from Medicare, from Medicaid.These are all debts that will come due that will have to be paid by the government, and eventually this fiscal deficit will lead to a government debt that will then, because of its increasing size lead to sharply rising interest burden.

In other words, in ten years time I would estimate that between 30 and 50% of tax revenue will be spent on the interest payments on the government debt. That will necessitate the monetization of the debt and that will then lead to a weak dollar.[….]

Esattamente quello che succederà e che la gente comune all’inizio non percepirà affatto.

Per inciso, ieri GS è stato il miglior titolo nel comparto finanziario USA.

E mentre ogni correlazione fra il $ ed i listini azionari è ormai finita :

La percentuale degli ottimisti sta ancora una volta aumentando a vista d’occhio.

Ma le commodities sembrano essere arrivate ad un punto di svolta, ecco ad esempio il Copper, già citato più volte, che sembra sempre di più mostrare una configurazione bearish :

Ed un occhio all’indice cinese , lo Shanghai Composite :

Che non pare avere al momento una grande tonicità, al contrario degli USA e degli europei.

Una Cina che ancora una volta ha confermato le (fantasiose ed irreali) cifre di crescita per il 2010 :

The government is targetting growth of 8% this year

Consumer price inflation will be kept at around 8%

The government is targeting new loans of CNY7.5 trillion, down from 2009’s record CNY9.59 trillion:

M2 growth in 2010 is targeted at 17%

Le lezioni del passato non sono state ancora imparate, pare.

")