Ieri sera i mercati USA hanno chiuso sui minimi di seduta, tornando esattamente sui valori pre bail-out Dubai.

La parte più interessante però ieri è stata sicuramente sul fronte macro :

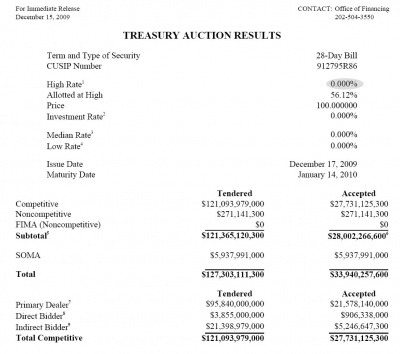

Per la seconda volta in una settimana , un asta di T-bonds USA ha chiuso come rendimento esattamente a zero.

Un processo che può andare avanti all’infinito, senza alcun dubbio.

Ma in questo modo come può essere risolto il problema del disavanzo pubblico e del deficit USA ?

In nessun modo, e lo stanno capendo infatti i cittadini USA, che hanno dato un verdetto inequivocabile :

[…]In a poll on Fox News, with over 163 thousand people voting, the vast, vast majority, or 99% of poll respondents are against raising the debt ceiling, claiming “This out-of-control spending is outrageous and irresponsible.”[…]

Una percentuale che in altri tempi si sarebbe definita bulgara, solamente il 99% si è mostrato contrario alla attuale politica economica USA.

Per altro, pare che la tanto sbandierata ripresa sia finita su di un binario morto :

Empire State Manufacturing Continues Plunging, Drops From 23.5 To 2.55 In November, 34.6 In September

Interessante leggere il commento :

[….]The indexes for new orders and shipments posted somewhat more moderate declines but also moved close to zero. Input prices picked up a bit, as the prices paid index rebounded to roughly its November level ; however, the prices received index moved further into negative territory, suggesting that price increases are not being passed along.

Current employment indexes slipped back into negative territory.

Future indexes remained well above zero but signaled somewhat less widespread optimism than in recent months. Indexes for expected prices paid and received declined moderately but remained well above zero.[…]

Che tristezza vedere gli Stati Uniti in queste condizioni.

Sempre riguardo l’ottimismo, che pare svanito fino alla prossima release del Quantitative easing 2.0 :

[…]Manufacturers remained generally optimistic about the outlook for general business conditions and activity, although a bit less so than in recent months.

After rising to its highest level in more than a year, the index for expected general business conditions retreated 14 points to 43.0—still a high level but the lowest since July.

The forward-looking indexes for both new orders and shipments fell by almost as much but remained in the upper 30s, while the future unfilled orders index declined by a more moderate 5 points to 12.0.

The index for expected delivery times edged up to zero, its highest level in more than a year, and the measure for future inventories was unchanged at 7.9.[…]

Naturalmente, in una situazione del genere i margini operativi aziendali stanno sempre più assottigliandosi :

[….]Manufacturers See Margins Squeezed Survey respondents faced somewhat higher input prices in December, while their selling prices declined.

The prices paid index rose 9 points to 19.7, reversing a drop of similar magnitude in November and suggesting some renewed price pressures.

At the same time, the prices received index slipped 6.6 points to -9.2, its lowest level since August. Employment indexes declined for the second straight month, falling below zero for the first time in a few months: the index for number of employees slipped 7 points to -5.3, and the average workweek index fell 11 points to -5.3.[….]

Poco da aggiungere, se non che questo è un fatto che sto segnalando da mesi.

E naturalmente le condizioni generali di business sono ulteriormente peggiorate :

[…]The general business conditions index fell from 23.5 to just 2.6, suggesting a leveling off in conditions after four straight months of improvement.Roughly 24 percent of those surveyed in December said that conditions had improved, while 22 percent reported that conditions had deteriorated.

Most of the other specific activity measures fell a bit less sharply: the new orders index slipped more than 14 points to 2.2, and the shipments measure declined by just under 7 points to 6.3.The unfilled orders index fell by more than 18 points to -21.1, its lowest level in nine months.

In contrast, the index for delivery times held steady at -2.6, and the inventories index, at -18.4, was little changed for the third straight month.[…]

Qualcuno ha ancora dei dubbi che questa è una ripresa solo sulla carta e che di reale non c’è proprio nulla ?

Per altro, le banche – sia d’affari, sia quelle commerciali – continuano a non fare circolare il denaro e – di fatto – continuano a bloccare ogni possibilità di ripresa del finanziamento, sia aziendale, sia privato.

Ma se questo collo di bottiglia non si stappa velocemente, i mercati, già di per sè su questi livello solo perchè sostenuti da fondi governativi e non certo perchè i fondamentali stiano rispecchiando il reale andamento dell’economia, rischiano rapidamente di girare ancora una volta – nonostante il Quantitative easing 2.0 alle porte – verso una nuova fase ribassista.

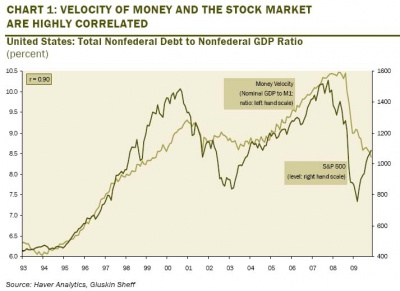

Il seguente grafico ci spiega il perchè :

Evidentissima, infatti, la correlazione fra la velocità di disponibilità di fondi e l’andamento dell’indice S&P500.

Se non verrà in qualche modo sostenuto il credito disponibile, il mercato di nuovo girerà verso sud, o quantomeno inizierà una lunghissima fase laterale, sulla falsariga di quanto visto in questi ultimi mesi.