E’ assai interessante notare che negli ultimi giorni – in corrispondenza di dati macro all’apparenza molto buoni (55.7 ISM USA, PMI Europa 52.6), i mercati hanno sempre reagito – tranne questa mattina, ma era scontato – con dei sell-off .

E se è vero che a partire dal Q3 2009 si stanno facendo sentire i massicci piani di stimulus forniti nei mesi scorsi dai vari governi per rilanciare l’economia (il cui costo si ripercuoterà pesantemente nei prossimi dieci anni su tutti noi), è altresì evidente che la frase di Rosemberg (” We are borrowing from the future “) suona come un monito importante al fatto che questo possa essere il top della ripresa (almeno finchè non saranno annunciati nuovi ulteriori piani di stimolo).

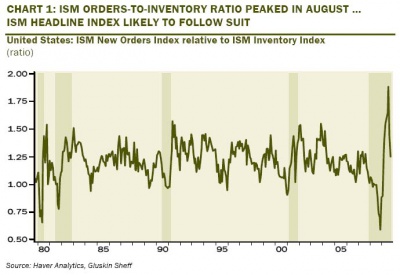

E’ interessante riportare quello che dice a riguardo Rosemberg :

[…]ISM is following a very similar pattern as it did in the aborted 2002 recovery year, again led by a brief spurt of automotive-related growth. What caught our eye in the report was the decline in the new orders–to-inventories ratio — to its lowest level since February (1.25x from 1.43x in September and 1.89x in August) [….]

Ed inoltre :

[…]The S&P 500 was already effectively pricing in a 59.0 level in the ISM index, so it will be interesting to see if this data-based rally is any more sustained than what we saw coming out of the better-than-expected GDP report last week. This market still has plenty of “growth” priced in.[…]

Ed infatti :

With all deference to the ISM index, the regional surveys have, for the most part, not validated the strong message from the national figure:

Boston’s Purchasing Managers’ Index (PMI) fell to 44.9 from 47.52.

Chicago’s PMI rose to 54.2 from 46.13.

New York’s PMI index sagged to 60.8 from 72.9

Cincinnati’s PMI edged up to 44.6 from 44.5.

Milwaukee’s PMI fell to 50 from 58

Richmond Fed index down to 7 from 14

Kansas City Fed production index slipped to 6 from 16

Texas manufacturing index worsened to -14.3 from -6.49.

The Southeast Michigan business activity index slid to 51.3 from 62.5.

Solamente due regioni hanno quindi migliorato il loro consenso, e le altre sette invece sono peggiorate.

Ma l’indice è salito.

Segnalo inoltre che – come nel 2007 – Blackstone ha molto probabilmente centrato il massimo di periodo.

Naturalmente non può fare una nuova IPO su se stessa, e quindi sta cercando di piazzare sul mercato società come AEI, una specie di Enron moderna .

Ma è una operazione che non è andata a buon fine :

[….]AEI, a former Enron entity with energy-infrastructure operations in 19 developing countries, had expected shares to price between $14 and $16 per share.

The company was offering 16.7 million shares. Its largest shareholder, Ashmore Funds, planned to sell 33.3 million.

Thursday, AEI lowered its expected price to $12 to $13 per share.

It raised its offering to 20 million shares, while Ashmore Funds cut its offering to just 1 million shares.[…]

Oppure come AVIV reit (società operante nel real estate).

Peccato che entrambe le operazioni siano state abortite per questo motivo :

[…]We have decided not to proceed with an initial public offering of our shares at this time due to market conditions[…]

Ma se non ci riescono ora dopo un rally da più del 60% dai minimi e con una economia che sulla carta dà segni di grande ripresa (ma solo sulla carta) quando riusciranno nel loro intento ?

")