Oggi iniziamo la analisi del periodo pre-pasquale con due fatti che sono stati oscurati dal dato – invero poco significativo e fuorviante, ma di ciò ci occuperemo in seguito – del Non Farm Payroll, in miglioramento, certo, ma molto inferiore alle attese.

Ben pochi commentatori infatti hanno prestato attenzione alla improvvisa mossa della Banca Centrale Svizzera a sostegno dell’€ Giovedì alle ore 18.00, poco dopo la chiusura dei mercati europei :

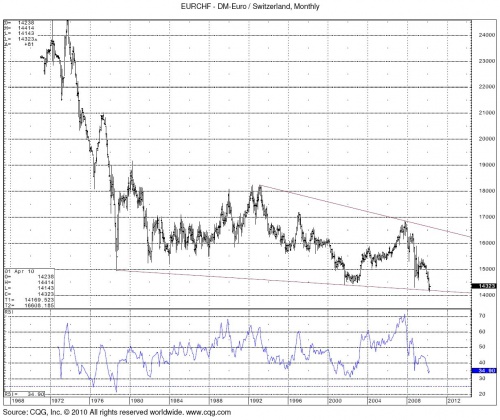

Un vero e proprio blitz, mentre sembrava fino a quel punto che la valuta unica europea stesse involandosi ancora una volta verso un ulteriore minimo storico nei confronti del CHF.

Il grafico di lungo periodo in effetti parla chiarissimo, ma è facile notare che nel breve è attesa una ulteriore reazione dell’€.

Ed in caso di ulteriore intervento della SNB il target è 1.46-1.47, anche se sinceramente per il momento è difficile fare previsioni.

Non dimentichiamoci però che – in caso di inasprimento della crisi greca, il CHF può essere visto – as usual – insieme al Gold come valuta rifugio, di esempi del genere nella storia ce ne sono davvero molti.

Naturalmente, di riflesso l’€ ha momentaneamente rimbalzato anche contro USD, tornando in area 1.35-1.36.

Goldman Sachs nel frattempo pubblicamente ricambia per la terza volta in un settimana il parere :

The Euro will likely remain stuck between two largely offsetting forces.

Cyclical acceleration in the Eurozone and deceleration in the US, external balances and the outlook for earlier monetary policy normalisation by the ECB all suggest upside risks for the Euro.

But on the other hand, the uncertainty about Greece and, more importantly, about the institutional set-up of the Eurozone will command a high fiscal risk premium for the foreseeable future.

We have revised down our 3mth and 6mth forecasts to the same level as our old 12mth forecast, 1.35 flat. Other forecasts are affected through the Euro crosses.

Pare molto strano che i maghi di GS abbiano sbagliato per la terza volta, soprattutto perchè giovedì pomeriggio, in piena spike rialzista, sono stati pescati a vendere – come probabile operazione di hedging – diversi large S&P :

Goldman Selling Several Thousand S&P Large Contracts @ 1177

La fonte pare molto attendibile, nientemeno che Ben Bernanke.

Ma quale può essere la motivazione – oltre che tecnica – di questa operazione di Goldman Sachs ?

Pare che – nonostante le dichiarazione di facciata – la FED stia per ritoccare all’insù il costo del denaro, forse addirittura oggi in giornata :

It is anticipated that a closed meeting of the Board of Governors of the Federal Reserve System at 11:30 a.m. on Monday, April 5, 2010, will be held under expedited procedures, as set forth in section 26lb.7 of the Board’s Rules Regarding Public Observation of Meetings, at the Board’s offices at 20th Street and C Streets, N.W., Washington, D.C.

The following items of official Board business are tentatively scheduled to be considered at that meeting.

Meeting date: April 5, 2010

Matters to be Considered :

1. Review and determination by the Board of Governors of the advance and discount rates to be charged by Federal Reserve Banks.

A final announcement of matters considered under expedited procedures will be available in the Board’s Freedom of Information and Public Affairs Offices and on the Board’s Web site following the closed meeting.

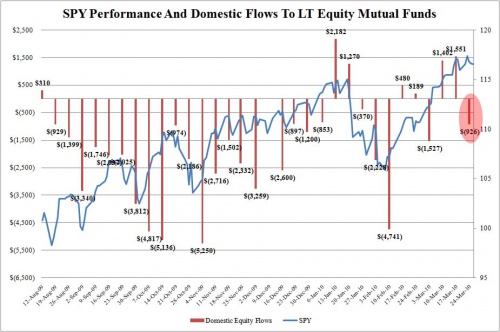

Questo spiegherebbe molte cose, anche il seguente grafico :

Fund flows for domestic equity mutual funds turned negative for the week of March 24 to the tune of almost $1 billion, after a substantial spike the week before.

Fondi sostanzialmente in uscita dal mercato in una settimana di rialzi, fatto abbastanza sospetto che ci dà un ulteriore campanello di allarme sul breve (naturalmente nel lungo il bull market al momento non è per nulla in discussione).

E che le pressioni inflazionistiche – come già segnalato più volte – inizino a farsi sentire, lo conferma il fatto che il Crude ha rotto – naturalmente al rialzo – il trading range in cui era ingabbiato da mesi ; e guardando il grafico di lungo periodo, viene un brivido, non tanto ai trader, ma ai consumatori : Pressioni inflazionistiche + crescita modesta + discoccupazione sempre marcata = stagflazione alle porte ?

Stiamo a vedere, ma lo scenario che si sta delineando per il futuro pare sempre di più questo.

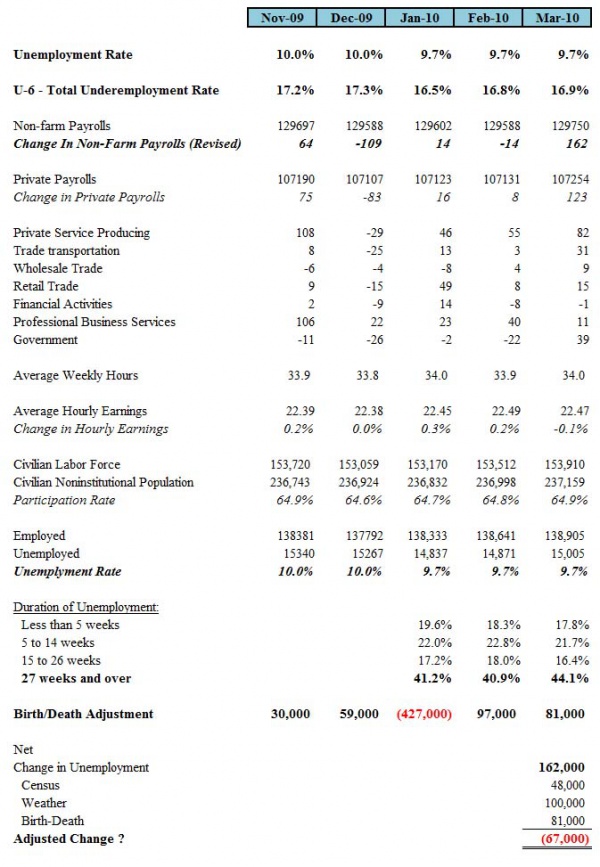

E finalmente arriviamo al NFP, ecco il riassunto dei dati globali :

Significativo il seguente commento :

The 162k increase in nonfarm payrolls reported for March looks like it is mainly due to the hiring of temporary workers for the census (+48k) and weather effects.

While the latter can only be estimated, our +100k figure looks right if not a bit low based on three observations:

(a) an increase in construction payrolls (+15k vs declines of 60k in Jan and 59k in Feb),

(b) a full recovery from Feb setbacks in workweeks,

and (c) a sharp swing down in the number of people reporting themselves as out of work due to weather (to 135k in Mar from 1.03 million in Feb, which statistically would be consistent with a weather effect of more than 100k).

E soprattutto :

Despite the firmer tone of the household survey, the unemployment rate remained at 9.7%, as labor force participation edged up for a second consecutive month.In fact, on an unrounded basis the unemployment rate came just short of rising 0.1 (9.749%).

Meanwhile, the broadest “U6” measure of underemployment edged up 0.1 point, to 16.9%, underscoring the fact that there is still quite a bit of unused capacity in the labor market, both in terms of people who are working part time because they cannot find full-time work and in those who have not reentered the labor force.

Consistent with this, average hourly earnings continue to weaken, slipping 0.1% on the month and dragging the year-to-year trend down to 1.8% (despite a small upward revision to the prior month).

With the recovery of workweeks in March, the index of total hours worked rose 0.4%.

For the quarter as a whole, hours worked were up 2.1% at an annual rate. With the “bean count” for real GDP still fairly consistent with our estimate of a 2.5% annualized increase, the implication is that productivity gains have diminished sharply.

Una volta tanto, un commento significativo da parte di GS, che di fatto afferma che la recessione NON è finita, e che soprattutto la disoccupazione è rimasta stabile, sono stati recuperati ben pochi posti di lavoro, molto meno di quelli che il modello del BLS ha previsto.

E che – soprattutto – il tasso è rimasto pressocchè stabile, ed il GDP deve essere rivisto al ribasso.

Anche questo un altro dato significativo, un’ altra tessera al mosaico che si sta viavia delineando nel corso del tempo, che ci dà ancora una volta un’altra conferma di ciò che ci aspetta.

Nel frattempo, i bonds hanno momentaneamente ceduto tornado sul “solito” supporto :

Naturalmente pronti a rimbalzare come una molla nel caso di aumento del costo del denaro sin addirittura da oggi.

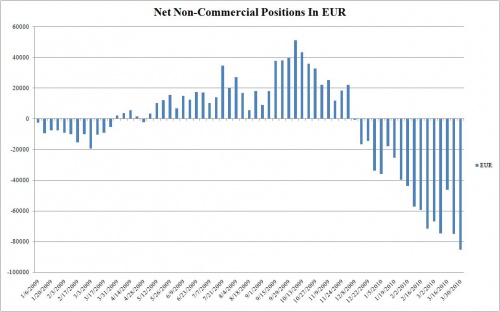

Mentre l’opera di restaurazione del carry-trade in stile estate 2007 pare essere arrivata a buon punto :

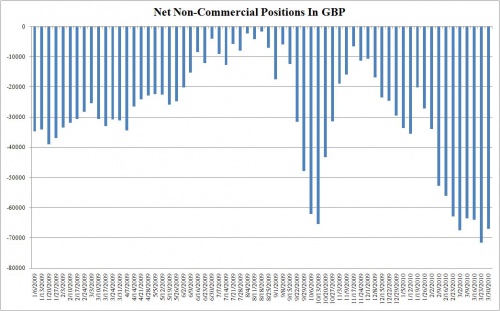

The carry trade rout is accelerating, even as the euro keeps hitting new spec short records.

After the prior week’s (March 23) net short exposure hit a new record of -74,917, net euro shorts hit a new all time record of -85,326.This is occurring even as the cable saw last week’s record shorts of -71,624 tighten marginally to just -67,073.

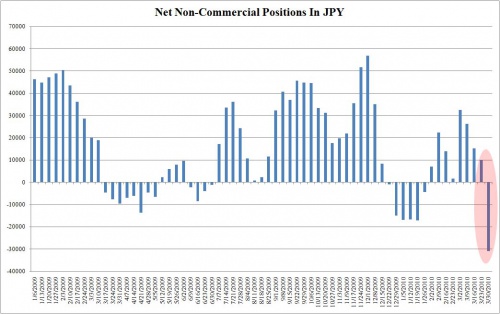

Yet the biggest stunner was the whopping collapse in Yen net short positions, which moved from +10,161 to -30,866: the biggest net short in the Japanese currency since 2007.

This is happening just in time for the Yen to hit fresh 7 month lows against the dollar, as the Yen is back to being the funding currency for all carry trades.

The one currency which is openly being sold by its central bank, the CHF, saw shorts increase by 5.5k from -1,088 to -6.540.

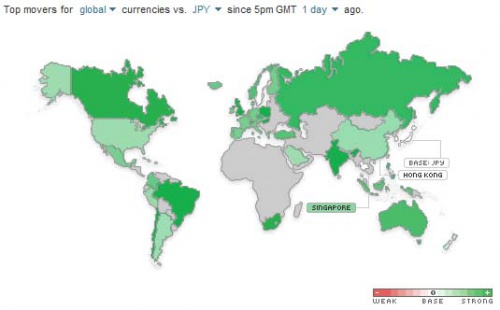

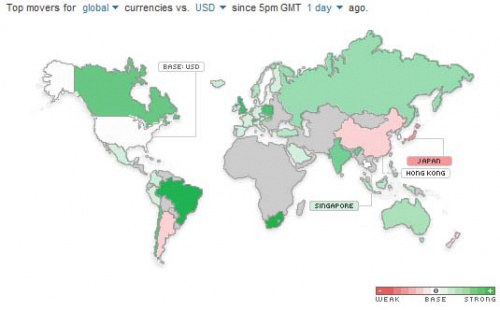

Ed infatti, guardando la mappa mondiale degli spostamenti nel Forex dello scorso giovedì, è possibile notare esattamente questo tipo di impianto :

")

")