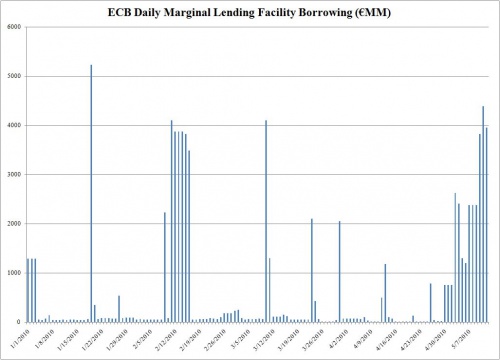

The ECB’s equivalent of the Discount Window, the Marginal Lending Facility, has seen a spike in borrowings over the past two weeks. As of May 12, total borrowings were €4 billion, after hitting €4.4 billion the night before, the second highest amount borrowed by European banks since an errant print of €5.2 billion in January 19, which was more of a liquidity rebalancing instead of an actual indication of short-term liquidity demand.

As we disclosed previously, we are keeping a close eye on this indicator as it is the best determination of the funding and liquidity problems gripping Europe. And as the chart shows, beginning in May, more and more banks are now relying on the ECB for overnight liquidity.

Situazione potenzialmente molto pericolosa, come infatti ci mostra il seguente grafico.

Prossimi problemi di liquidità in Europa ?

D’altra parte, la sorte dell’€ è appesa ad un filo, e tutte le decisioni che devono essere presa da questo momento in poi sono esclusivamente di tipo politico :

There is a way out of this crisis, but it is not the policy of wage deflation imposed on Ireland, Greece, Portugal, and Spain, with Italy now also mulling an austerity package.

This can only lead to a debt-deflation spiral.

The IMF admits that Greece’s public debt will rise to 150pc of GDP even after its squeeze, and that Spain’s budget deficit will still be 7.7pc of GDP in 2015.

The only viable policies – short of breaking up EMU or imposing capital controls – is to offset fiscal cuts with monetary stimulus for as long it takes. Will it happen, given the conflicting ideologies of Germany and Club Med ?

The ECB denies that it is engaged in Fed-style quantitative easing, vowing to sterilise its bond purchases “euro for euro”. If they mean it, they must doom southern Europe to depression.

No democracy will immolate itself on the altar of monetary union for long.

Queste sono le parole del sempre lucido Ambrose Evans-Pritchard, le cui domande hanno una sola risposta : la BCE per garantire la sopravvivenza dell’€, dovrà garantire un perpetuo QE, ed è chiaro che alla lunga il gioco porterà al massacro.

Ed ecco allora perchè la sempre lungimirante Goldman Sachs consoglia di vendere il Gold ai suoi “migliori”clienti (ed è chiaro invece che vuole fare scendere le quotazioni per accumulare, of course) :

The recent market turmoil helped propel gold prices back above $1200/toz in recent days as investors increasingly looked for safe havens amidst heightened concerns over Greece and the potential for financial contagion to other European countries.

The sharp rise in the level of concern over Europe can be seen in the credit default swap (CDS) markets where cost to insure against sovereign default by Greece, Spain, Portugal, and Italy spiked to the highest levels on record (see Exhibit 21).

Interestingly, USD-denominated gold prices rallied sharply higher off of these concerns despite the fact that these concerns also helped push the euro to its lowest levels in more than a year

Ben poco da aggiungere, se non che il Bull market del Gold è certamente lontano dal suo termine, anche perchè il Gold è destinato a divenire – quantomeno simbolicamente – l’unica divisa di riferimento mondiale

Aspettiamoci una correzione anche di qualche punto per il Gold, ma non dimentichiamoci i target ambiziosi, anche perchè in chiusura di venerdì è stato raggiunto il massimo degli ultimi 10 anni.

Una regola dettata dall’esperienza pratica e da studi tecnici, che va contro il modo di pensare comune, ma che è alla base di molti comportamenti della nostra esistenza.