Ecco cosa ci hanno detto i mercati negli ultimi giorni, iniziamo dalla minaccia persistente di deflazione :

Dati pessimi, come per altro non ha mancato di sottolineare Zerohedge :

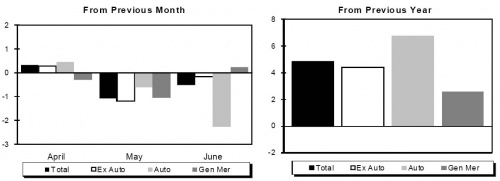

The deflation threat continues as the drop in total retail sales persists, with the latest number coming in at -0.5%, once again worse than expectations of -0.3%, compared to a prior revised number of -1.1%.

Ex autos come in at -0.1%, in line with expectations. The biggest plunge was in “Motor vehicle & parts dealers” which plunged 2.3% in June.

Inoltre :

Empire manifacturing index, un disastro :

The Empire Manufacturing Index plunged to 5.08 on expectations of 18, and previously at 19.57 !

The stunning drop was driven by a contraction in virtually all diffusion categories : New Orders (10.13 from 17.53), Shipments (6.31 from 19.67), Unfilled Orders (-15.87 from -1.23), Delivery Time (-7.94 from 9.88), Prices Paid (25.40 from 27.16), Prices Received (-1.59 from 4.94), and Average Employee Workweek (-9.52 from 8.64).

Only inventories increased marginally (we may have seen this before), from -1.23 to 6.35. All in all a disaster.

PPI, sulla stessa falsariga :

Elsewhere the PPI also plunged much more than expected, coming in at -0.5 on expectations of -0.1 as deflation is now pervasive. In all fairness, core PPI came in as expected at 0.1%.

Initial jobless clains, no comment :

The Initial Jobless Claims came in at 429,000 from 458,000 the week before, a number made irrelevant after various automakers announced they would continue summer production in autoplants that otherwise get shutdown for the period, thus skewing the seasonal adjustment.

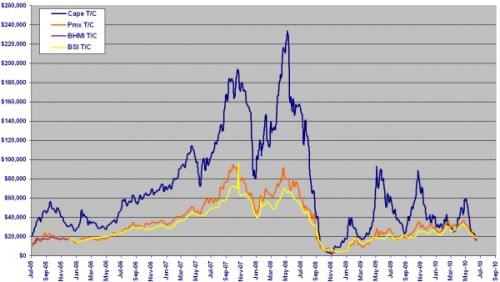

Baltic Dry Index, si commenta da solo, 35 sedute di fila in calo :

Dulcis in fundo ,ECRI Leading Economics Index ancora in netto calo , double dip recession sicura al 100% se raggiunge il valore di -10, ed ora siamo solamente a -9.8 :

Un bel quadretto, non c’è dubbio.

Inoltre sul fronte economico/finanziario , in attesa degli stress test, sono arrivate le seguenti notizie :

Illinois : default risk maggiore dell’Islanda (e tutti sappiamo cosa è successo nel 2008 in questo paese).

FOMC : non ci sarà ripresa sostenuta prima di 5-6 anni, mentre in tv il teleimbonitore parla di fortissimo rilancio dell’economia.

Participants generally anticipated that, in light of the severity of the economic downturn, it would take some time for the economy to converge fully to its longerrun path as characterized by sustainable rates of output growth, unemployment, and inflation consistent with participants’ interpretation of the Federal Reserve’s dual objectives ; most expected the convergence process to take no more than five to six years.

JPMorgan , una bomba ad orologeria ?

Goldman Sachs , ridicolo risarcimento di 550Mln di $ per l’ormai famoso caso di truffa del 2008, notizia fatta uscire giovedì sera – in concomitanza con l’altra ridicola news su BP che finalmente (?!) avrebbe temporaneamente toppato la falla nel golfo del Messico (dopo solamente qualche mese) :

BP has succeeded in capping the well and stopping oil from flowing into the Gulf of Mexico…at least temporarily.

Due notizie che hanno avuto il sapore del sell the news (anche perchè fra le altre venerdì c’è stata la pessima trimestrale di General Electric) , ecco cosa è successo agli indici :

Spoore mercoledì.

Giovedì.

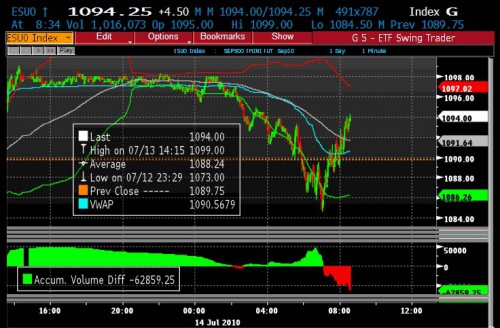

Venerdì, credo che l’andamento nell’intraday lo si legga perferttamente.

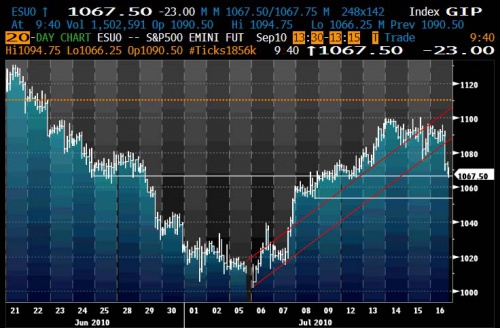

E guardando pure il daily in dettaglio, la situazione non pare certo positiva :

Ed il Nasdaq tiene relativamente solo per il peso massimo Apple, ed ecco perchè Steve Jobs si è scusato in diretta televisiva in tutto il mondo per i problemi dell’ Iphone4, mica solo per una questione solo di immagine, ma ne va della tenuta del Nasdaq 100 :

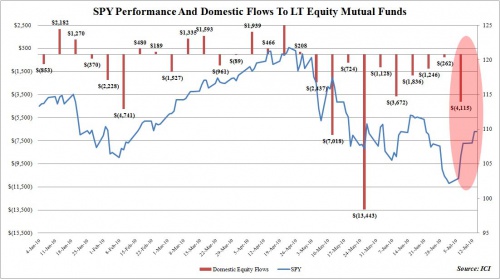

Ed intanto i fondi continuano ad uscire ed non certo ad entrare nell’azionario :

In the week ended July 7, ICI reports that domestic equity mutual funds saw $4.1 billion in outflows, the largest outflow in the past 2 months, and the third biggest weekly redemption in 2010! This is also the tenth sequential outflow, amounts to $34 billion in total outflows YTD, and represents a losing streak even worse than that of the BDIY.

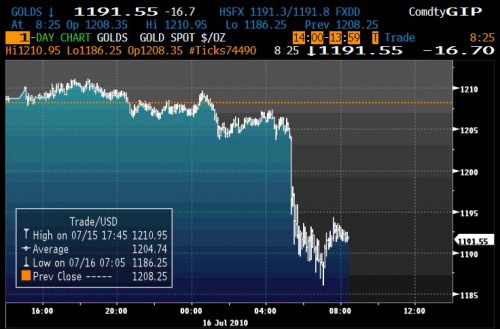

Il gold collassa per le solite prese di beneficio forzate :

Paulson deve fare cassa, e velocemente, ecco il motivo del forte ribasso, non imputabile certo ad altre cause tecniche, come ancora una volta ci ricorda Zerohedge :

Paulson ha le maggiori posizioni su BAC e C, venerdì collassate, di quanto è sotto in questo momento ?

With a holding of 168 million shares of BAC and 506 million in Citi, Paulson and Co. is down nearly $300 million on just its top two positions alone.

When one adds the other top ten positions, which include $3.5 billion worth of GLD, as well as massive positions in ANG, CMCSA, STI, TRE, RIO, BSC, COF, WFC, MGM and many others, it is not surprising that the market is rife with rumors that the once vaunted bearish and now very much bullish (who according to Goldman’s carefully crafted settlement press release yesterday, only achieved his subprime-related wealth due to prospectus misrepresentations by Goldman, which is now permanently in the public record) is down about $1 billion for the day so far.

L’unica cosa che stona in tutto questo quadro sono le pessimistiche previsioni di Goldman Sachs :

Per una volta starà dicendo – finalmente – quello che pensa realmente ?

")