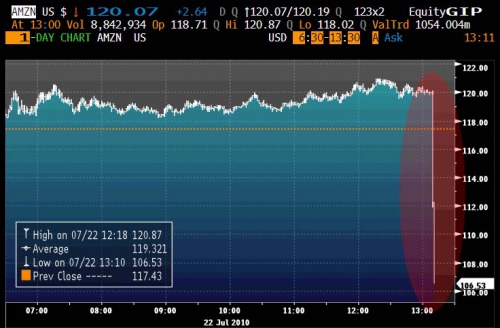

Ieri indici al galoppo, con sorpresa finale, i risultati deludenti di AMZN con conseguente crollo in AH :

Per altro – e qua non ho avuto nei giorni scorsi il coraggio di segnalarlo – le maggiori possibilità di prolungato movimento in caso di nuova gamba al rialzo stanno in Asia, sponda Nikkei :

Dove sto tentando da qualche gg i maggiori acquisti (oltre all’ASX).

Ed anche al Bovespa :

Ed anche qua attenzione, il comportamento del”ETF ECH, unico da un paio di settimane in trend rialzista confermato dai TS (oltre anche a TUR, quasi tutti gli ETF sulle commodities ed a molte valute esotiche contro $, come BZF e BNZ) paiono sottointendere che ci può essere un rally estivo.

Copper vicino ad una resistenza chiave.

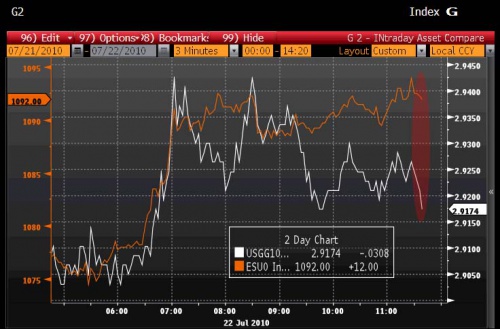

Ed è da segnalare la divergenza a livelli massimi fra Spoore e 10Yr T-Bond :

Il che significa che non c’è affatto travaso fra i fondi dall’obbligazionario all’azionario o viceversa, ma semplicemente molti preferiscono stare liquidi.

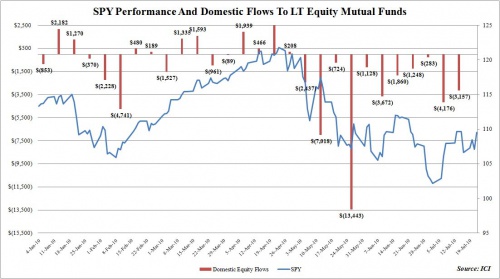

La conferma arriva anche da qua :

11a settimana di uscita consecutiva di fondi dallo Spoore, ma nel frattempo +90 punti.

Tutti segnali di deflazione in effetti questi ultimi così come quello ieri ignorato :

Inventory of existing homes available for sale rose to 3.99 million, representing an 8.9 month supply at the current sales pace. This is up from 8.3 months in May, and is the worst number since August 2009, when it was at 9.2 months.

Ed oggi risultati degli stress test, che arrivano dopo che ieri è stata dipinta una situazione davvero rosea per l’economia europea, dati davvero ottimi :

Euro-Zone Industrial New Orders SA for May 3.80% m/m 22.70% y/y higher than expected Consensus -0.10% m/m 20.00% y/y Previous 0.60% m/m 21.90% y/y (Revised from 0.90% m/m 22.10% y/y).

France Business Confidence Indicator for July 98 higher than expected Consensus 94 Previous 96 (Revised from 95).

France Own-Company Production Outlook for July -9 lower than expected Consensus -7 Previous -7.

France Production Outlook Indicator for July -2 higher than expected Consensus -6 Previous -4.

France Consumer Confidence Indicator for July -39 higher than expected Consensus -40 Previous -39.

France PMI Manufacturing for July 53.7 lower than expected Consensus 54.1 Previous 54.8.

France PMI Services for July 61.3 higher than expected Consensus 60 Previous 60.8.

UK Retail Sales Ex Auto Fuel MoM and YoY for June 1.00% m/m 3.10% y/y higher than expected Consensus 0.60% m/m 2.40% y/y Previous 0.70% m/m 2.90% y/y (Revised from 0.50% m/m 3.40% y/y).

UK Retail Sales w/Auto Fuel MoM and YoY for June 0.70% m/m 1.30% y/y higher than expected Consensus 0.50% m/m 1.00% y/y Previous 0.80% m/m 1.70% y/y (Revised from 0.60% m/m 2.20% y/y).

Sell the news oppure continuazione ad libitum della gamba al rialzo ?